Since the worth of the property is an important factor in understanding the danger of the loan, identifying the value is a crucial element in home mortgage loaning. The worth may be identified in numerous ways, but the most typical are: Actual or deal worth: this is usually required the purchase cost of the residential or commercial property.

Appraised or surveyed worth: in a lot of jurisdictions, some type of appraisal of the worth by a certified expert prevails. blank have criminal content when hacking regarding mortgages. There is often a requirement for the lending institution to get an official appraisal. Approximated value: loan providers or other celebrations might use their own internal price quotes, especially in jurisdictions where no authorities appraisal treatment exists, however also in some other circumstances.

Common denominators include payment to income (home mortgage payments as a portion of gross or earnings); financial obligation to earnings (all debt payments, including mortgage payments, as a percentage of earnings); and numerous net worth measures. In numerous countries, credit history are used in lieu of or to supplement these measures.

the specifics will differ from location to area. Income tax incentives generally can be used in forms of tax refunds or tax reduction plans. The very first implies that earnings tax paid by specific taxpayers will be refunded to the level of interest on mortgage taken to obtain house.

Some lending institutions might likewise require a possible borrower have one or more months of "reserve assets" offered. Simply put, the debtor might be required to show the accessibility of sufficient possessions to pay for the real estate costs (consisting of mortgage, taxes, etc.) for a period of time in case of the job loss or other loss of earnings.

Numerous nations have a notion of basic or conforming mortgages that specify a perceived appropriate level of threat, which might be official or informal, and may be enhanced by laws, federal government intervention, or market practice. For instance, a basic home mortgage might be considered to be one without any more than 7080% LTV and no more than one-third of gross earnings going to mortgage debt.

What Beyoncé And These Billionaires Have In Common: Massive Mortgages - Questions

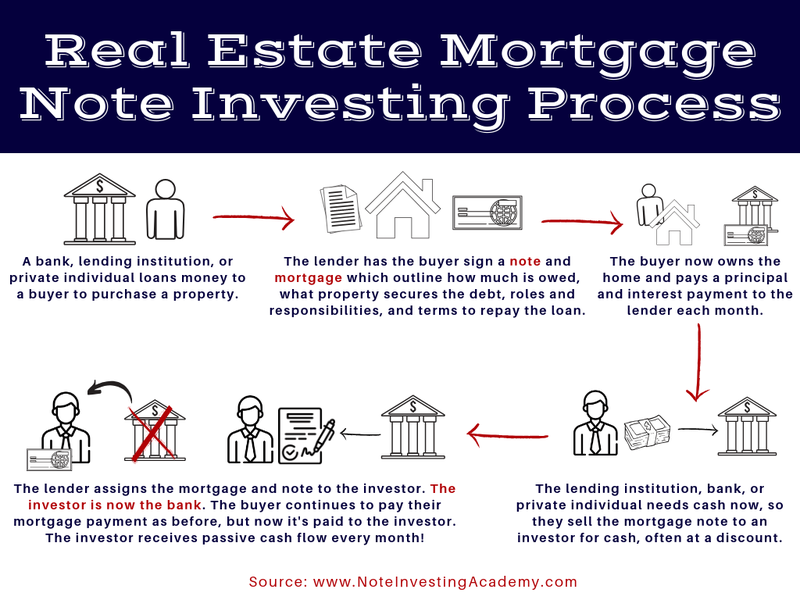

In the United States, a conforming home loan is one which fulfills the recognized guidelines and procedures of the two major government-sponsored entities in the real estate finance market (consisting of some legal requirements). In contrast, lending institutions who choose to make nonconforming loans are working out a greater threat tolerance and do so understanding that they deal with more obstacle in reselling the loan.

Regulated loan providers (such as banks) may undergo limits or higher-risk weightings for non-standard home loans. For instance, banks and home loan brokerages in Canada face limitations on providing more than 80% of the property value; beyond this level, mortgage insurance coverage is typically needed. In some countries with currencies that tend to diminish, foreign currency home loans prevail, allowing lending institutions to lend in a steady foreign currency, whilst the customer handles the currency risk that the currency will depreciate and they will for that reason require to convert greater amounts of the domestic currency to pay back the loan.

Total Payment = Loan Principal + Expenditures (Taxes & fees) + Total interests. Repaired Interest Rates & Loan Term In addition to the 2 standard ways of setting the cost of a mortgage (repaired at a set interest rate for the term, or variable relative to market interest rates), there are variations in how that expense is paid, and how the loan itself is paid back.

There are likewise different mortgage payment structures to suit various kinds of customer. The most common way to repay a protected mortgage is to make routine payments timeshare relief toward the principal and interest over a set term. [] This is frequently described as (self) in the U.S (mortgages or corporate bonds which has higher credit risk). and as a in the UK.

Certain information might specify to different locations: interest may be computed on the basis of a 360-day year, for example; interest might be intensified daily, annual, or semi-annually; prepayment penalties might apply; and other factors. There might be legal constraints on specific matters, and customer security laws might define or prohibit certain practices.

In the UK and U.S., 25 to thirty years is the typical optimum term (although much shorter durations, such as 15-year home loan, prevail). Home mortgage payments, which are typically made regular monthly, contain a repayment of the principal and an interest element. The amount going towards the principal in each payment differs throughout the regard to the home loan.

See This Report on How Many New Mortgages Can I Open

Towards the end of the home loan, payments are primarily for principal. In this method, the payment quantity determined at start is determined to make sure the loan is paid back at a specified date in the future. This provides debtors guarantee that by preserving repayment the loan will be cleared at a defined date if the rates of interest does not change.

Likewise, a home loan can be ended prior to its scheduled end by paying some or all of the rest too soon, called curtailment. An amortization schedule is usually exercised taking the principal left at the end of every month, multiplying by the regular monthly rate and after that deducting the month-to-month payment (what is the best rate for mortgages). This is normally generated by keywest timeshare an amortization calculator using the following formula: A = P r (1 + r) n (1 + r) n 1 \ displaystyle A =P \ cdot \ frac r( 1+ r) n (1+ r) n -1 where: A \ displaystyle is the routine amortization payment P \ displaystyle P is the principal amount obtained r \ displaystyle r is the rate of interest expressed as a fraction; for a regular monthly payment, take the (Annual Rate)/ 12 n \ displaystyle n is the number of payments; for regular monthly payments over 30 years, 12 months x 30 years = 360 payments.

This kind of home mortgage is common in the UK, especially when related to a routine investment strategy. With this plan routine contributions are made to a separate financial investment strategy designed to develop a swelling sum to pay back the home loan at maturity. This kind https://damienpose419.mozello.com/blog/params/post/2914413/what-is-the-concept-of-nvp-and-how-does-it-apply-to-mortgages-and-loans-can of arrangement is called an investment-backed home mortgage or is often related to the type of plan utilized: endowment home loan if an endowment policy is used, similarly a personal equity strategy (PEP) home loan, Person Savings Account (ISA) home mortgage or pension home loan.

Investment-backed home mortgages are seen as greater danger as they depend on the investment making adequate return to clear the debt. Until just recently [] it was not uncommon for interest only home mortgages to be arranged without a payment automobile, with the customer gambling that the home market will rise adequately for the loan to be paid back by trading down at retirement (or when rent on the home and inflation combine to exceed the interest rate) [].

The problem for many individuals has been the truth that no repayment car had been implemented, or the vehicle itself (e. g. endowment/ISA policy) carried out inadequately and therefore insufficient funds were readily available to pay back balance at the end of the term. Moving on, the FSA under the Mortgage Market Evaluation (MMR) have actually specified there must be rigorous requirements on the payment automobile being used.